- Playing For Doubles

- Posts

- PayPal: Average Business, Good Stock?

PayPal: Average Business, Good Stock?

An Average Business Can Still Be A Good Stock

Ahmad Jivraj

March 04, 2026

If you like this article, please share it with a friend ❤️. Thanks :)

Two weeks ago I wrote about how PayPal systematically squandered a decade of competitive advantages. PayPal was what I call a Stage 3 Maverick (A Leader), but has since lost its way. Apple Pay and Stripe ate their lunch. The Visa deal gutted their economics. Branded checkout is declining. They missed BNPL. They missed lending-as-infrastructure. They didn’t build their own rails. And they’re on their third CEO in three years.

All of that is still true.

But here’s the thing about investing: an average business can still be a good stock. Not because the business gets better, but because the price gets low enough that it doesn’t need to. And if the business does improve, that’s pure optionality.

PayPal at $42 billion is a very different proposition than PayPal at $350 billion was.

Let me explain why I’m starting to get interested.

The Ads Business Nobody Is Pricing In

PayPal has hired Mark Grether to build a new advertising business. If you don’t know Grether, you should. He came to Amazon Ads via acquisition, he was CEO of Sizmek, a demand-side platform Amazon acquired. Then he joined Uber and built their ads business essentially from scratch. That business just hit $2 billion in annual revenue this year.

He then chose to leave Uber for PayPal. That tells you something about the size of the opportunity he sees.

The logic is straightforward. PayPal sits on what they call the “transaction graph” - a cross-merchant view of how 430 million consumers actually spend money. Unlike Google’s intent graph or Facebook’s social graph, PayPal’s data is built on verified purchase behavior. What people bought, how much they spent, where they spent it, how often etc. As a result, PayPal doesn’t need cookies or proxies. They see real transactions across tens of millions of merchants (and this becomes even more important as Apple/Google lock down on online privacy).

This is the same kind of purchase signal that makes Amazon’s ad business generate better ROI than Google’s for many advertisers.

So how big could this get? Uber hit a $2 billion revenue run-rate in five years with roughly 200 million monthly active users. PayPal has double that user base. And the purchase signal is arguably more valuable to advertisers. It also spans the entire open web, not just rides and food delivery.

Here’s where it gets interesting for the stock. An ads business at PayPal would carry dramatically higher margins than the core payments business.

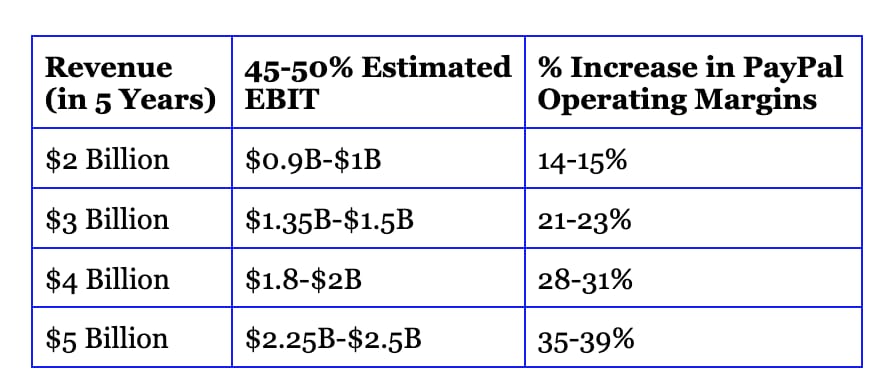

If we assume 45-50% EBIT margins on ads revenue, the impact on PayPal’s profitability is material. At $2 billion in ads revenue, that’s roughly $1 billion in incremental operating income, lifting company-wide margins by 14-15%. At $3 billion, you’re looking at over $1.4 billion and a 20%+ margin lift. Scale it to $4-5 billion and you’re fundamentally changing the profitability profile of the entire company.

These estimates assume zero growth in the rest of PayPal’s business. They’re purely additive.

Is $3-4 billion realistic? Grether built Uber’s business to $2 billion with 200 million users. PayPal has more than double that user base, and the purchase signal is arguably richer, it’s cross-merchant and transaction-verified. The question isn’t whether PayPal can build a meaningful ads business. It’s how big and how fast.

The market gives this almost no credit today because it doesn’t show up in the financials yet.

Strategic Value at a Clearance Price

When a company trades at $42 billion with 430 million accounts, checkout buttons on millions of merchant sites, a leading P2P brand in Venmo, and $6 billion in annual free cash flow, people start doing math.

And they have been. Bloomberg reported last week that Stripe is considering an acquisition of all or parts of PayPal. The talks are reportedly early-stage, but the strategic logic is compelling. Stripe has built the best payments infrastructure for the internet. But Stripe’s strengths are merchant-side and developer-facing. What they don’t have is a massive consumer brand, a 430-million-account wallet, or Venmo’s grip on younger consumers. PayPal fills every gap in Stripe’s consumer-facing ambitions. And the regulatory path would be cleaner than most combinations in this space, although still unclear.

JPMorgan is another logical buyer. Chase has spent years trying to build a meaningful consumer digital wallet. Chase Pay never scaled. PayPal would hand Jamie Dimon a 430-million-account digital wallet overnight, plus Venmo, a P2P Payments app with inroads with the exact millennial and Gen Z consumers Chase most wants to capture. JPMorgan’s balance sheet would let PayPal’s BNPL and credit products scale aggressively. Dimon has made no secret of his appetite for fintech market share, and unlike most names you could list, the regulatory path here actually looks manageable.

Then there’s private equity. An LBO might be more plausible than any strategic deal because it doesn’t require regulatory approval of a business combination: it’s just a change of ownership. The math is compelling: $6 billion in annual free cash flow against a $42 billion market cap implies roughly a 14% FCF yield. The playbook writes itself: cut costs (23,000+ employees leaves room), accelerate the ads business, monetize or spin non-core assets, exit in five years at a higher multiple.

Shopify is worth considering too. Their entire strategic ambition is to become the operating system for commerce, and PayPal fills their biggest gap: off-platform consumer reach. Shop Pay is growing fast but, PayPal’s checkout button lives on millions of merchant sites. Combine the two and you have a checkout presence that has massive reach. The data synergy is also compelling: Shopify’s merchant analytics layered on top of PayPal’s consumer purchase history would be extraordinarily valuable for both lending and advertising. And the regulatory risk feels low-to-moderate since there’s minimal overlap. This deal would meaningfully accelerate Shopify’s ambition to own the full commerce stack end-to-end.

I’m not interested in PayPal because I think it gets acquired. But at these prices, the M&A optionality is real and the market isn’t paying for it.

The Assets Are Still Growing

Lost in the doom narrative is that parts of PayPal are still performing well.

Venmo revenue grew approximately 20% last year to $1.7 billion. The platform has over 100 million active accounts. Venmo debit card monthly actives surged 43%. Pay with Venmo monthly actives climbed 24%. And here’s the kicker: only 5-10% of Venmo’s users currently use the debit card or Pay with Venmo features. Users who engage with these monetized products reportedly generate roughly 4x the revenue of those who don’t. If PayPal can convert even a modest percentage of that base, the revenue math changes significantly.

As a standalone company, Venmo at $1.7 billion in revenue growing 20% with a clear path to higher monetization would arguably command a premium valuation. You’re getting it essentially for free at today’s prices.

PayPal’s BNPL segment delivered over $40 billion in total payment volume in 2025, growing more than 20% year-over-year. Yes, they missed the chance to build a true consumer finance platform like Klarna or Affirm did. But the product exists, it’s scaling, and it contributes real economics.

PayPal is not a company in terminal decline.

Cheap and a Buyback Machine

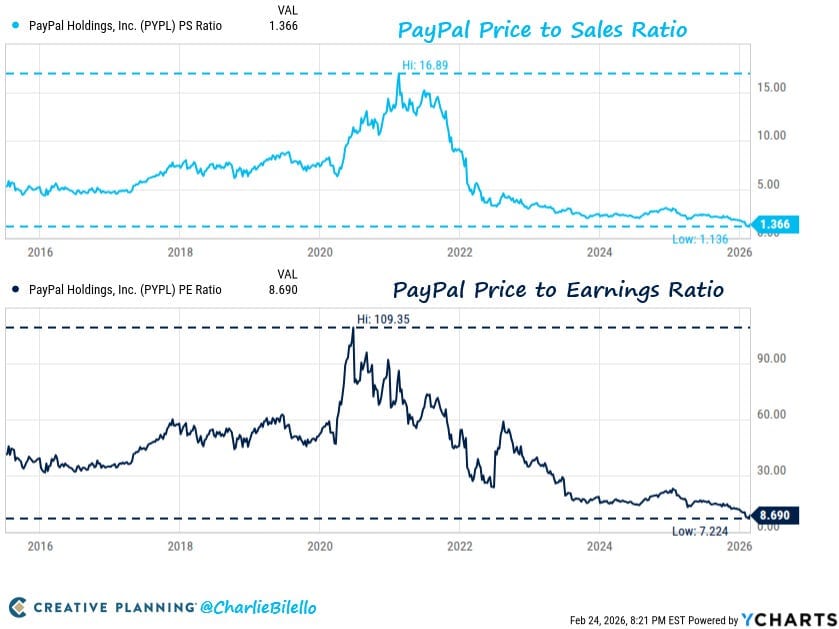

The stock is down roughly 85% from its 2021 highs. It used to trade at 17x sales. Today you can buy it for a little over 1x.

PayPal trades at roughly 8x earnings. The free cash flow yield is approximately 14-15%. This is not a business that’s hemorrhaging money. It’s a business the market has simply decided is low-growth, and priced accordingly.

Add to that significant capital returns. PayPal has committed to approximately $6 billion in annual share buybacks. That’s roughly 15% of the current market cap, every single year. Think about that for a moment. PayPal is buying back about one-seventh of itself annually at current prices. Since 2019, cumulative buybacks have already reduced the share count by about 20%. They also initiated their first-ever quarterly dividend earlier this year, a small $0.14 per share. Symbolic more than material, but it signals confidence in sustainable cash generation.

At this pace, the share count continues shrinking meaningfully. Even if operating income stays flat, EPS grows.

The Risks

Of course there are risks. You should know what you’re signing up for.

Branded checkout, historically the most profitable segment, is deteriorating. Growth decelerated to just 1% in Q4, down from 6% a year earlier. They’re on their third CEO in three years. Enrique Lores came from HP and took the role just days ago. He’s a seasoned operator, but he has no payments experience. The consumer environment is challenging, particularly for PayPal’s core lower-to-middle income demographic. And take rates continue compressing as the business mix shifts toward lower-margin Braintree and Venmo transactions.

The turnaround requires simultaneous execution across multiple fronts: reviving branded checkout, monetizing Venmo, scaling BNPL, building the ads business. That’s a lot to get right under a new CEO with no industry background.

These are real risks. I’m not dismissing them.

Why I’m Getting Interested

Because the stock price already reflects most of the problems above.

PayPal trades like a business in structural decline with no path forward. But it’s still generating $6+ billion in annual free cash flow, processing $1.8 trillion in total payment volume, and sitting on 430 million active accounts with checkout buttons across millions of merchant sites. And it has real optionality in ads and potential M&A that the market isn’t pricing.

At peak valuations in 2021, PayPal traded at a market cap to total payment volume ratio of roughly 15%. Today it’s 2.6%. Even a modest re-rate to 4-5% implies a dramatically different market cap.

Recall, there are three sources of return for any stock:

earnings growth,

multiple expansion, and

change in shares outstanding.

PayPal has a plausible path on all three:

Earnings growth: The ads business alone could lift operating margins by 20-30% within five years. That’s before any improvement in the core business.

+25% = 1.33x

Change in shares outstanding: At $6 billion in annual buybacks, we should see meaningful reduction in share count over the next few years, especially if the stock price stays depressed.

-20% = 1.25x

Multiple expansion: Even a modest re-rate from 8x to 10x earnings isn’t aggressive for a company generating this much cash. Higher margins from ads, improving sentiment, or any positive surprise in the core business could justify it. And 10x earnings is still cheap by almost any standard.

8x→10x = 1.25x

Combine all three and you can get to a double without particularly aggressive assumptions (1.33 * 1.25 * 1.25 = 2.08x)

All in all, PayPal is not a perfect business, and not a perfect story, but the price assumes the worst.

Reality is probably better than that.

Disclosure: I am considering a position in PayPal but do not currently own shares. Not Financial Advice.

If you enjoyed this post, please do share it with a friend.