- Playing For Doubles

- Posts

- Oil Stocks: Best Trade of the Next Few Years?

Oil Stocks: Best Trade of the Next Few Years?

Why oil stocks are set up for a major mean reversion.

Ahmad Jivraj

February 13, 2026

If you like this article, please share it with a friend ❤️. Thanks :)

If you’re new here, I share “buy-and-hold portfolios” that I think can double in 3-5 years. My investment philosophy is simple: Try to find the best stocks I can and let them sit for years.

Everyone talks about AI.

Nobody wants to talk about oil.

And that, right there, might be the opportunity.

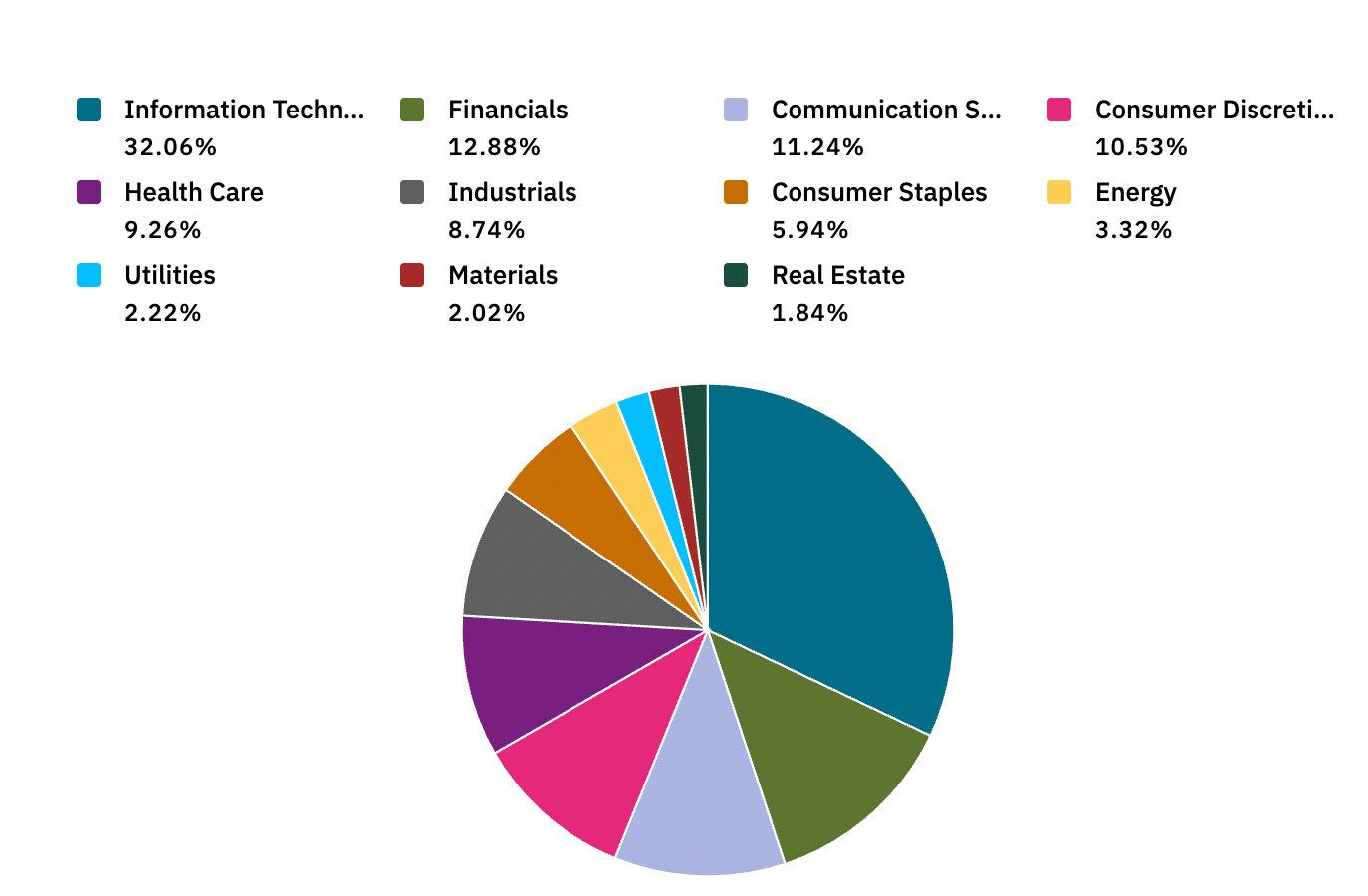

As of February 2026, the Energy sector makes up about 3.3% of the S&P 500.

That’s less than any single one of the top 5 stocks in the index.

The entire oil and gas industry, the stuff that literally powers the global economy, has been reduced to a rounding error in the most widely tracked index in the world.

This smells like a good setup: Not the thing everyone’s excited about, but the thing everyone has forgotten about.

Go Where Capital Is Scarce

I’ve written before about going where capital is scarce: It’s one of the most reliable investment frameworks I know.

When money floods out of a sector, what’s left behind are usually the survivors, companies with strong balance sheets, real cash flows, and the discipline to return capital to shareholders.

That’s exactly what’s happening in Energy right now.

Here’s the thing about mean reversion: It doesn’t care about narratives. It just happens.

Energy’s current ~3% weighting in the S&P 500 is near an all-time low.

At its peak in the early 1980s and again before the 2008 financial crisis, energy represented ~15% of the index. Even as recently as 2011, it sat at 12.6%.

Today, the sector’s weighting has shrunk by roughly 75% from that 2011 level.

Meanwhile oil and gas still accounts for roughly 80% of the world’s primary energy consumption!

Inflation: The Tailwind Nobody Is Talking About

Here’s where it gets interesting. We’re in a world where inflation has proven stickier than most people expected. Tariffs, reshoring, and fiscal deficits all point toward structurally higher inflation for years to come.

Oil companies love inflation. Their product, a commodity priced in dollars, naturally rises with inflation. Meanwhile, their biggest assets (reserves already in the ground, infrastructure already built) are relatively fixed cost. When the price of a barrel goes up, those incremental dollars flow almost directly to the bottom line. It’s a natural margin expansion machine.

This isn’t theoretical. During the inflationary 1970s, energy was the best-performing sector. During 2021-2022, when inflation spiked post-COVID, Energy was up meaningfully. While tech stocks were getting crushed, Exxon Mobil (XOM) returned over 80% in 2022 alone.

If you believe that inflation will remain high for much of the next 3-5 years, oil stocks provide a natural hedge that most portfolios are drastically underweight.

The Bear Case (And Why I Think the Bull Case Wins)

I’d be dishonest if I didn’t acknowledge the headwinds.

Renewable energy costs continue to fall.

ESG mandates have restricted capital flows into the sector for years.

EVs will continue to grow.

These are real forces.

But here’s my pushback:

The energy transition is going to take decades, not years.

Global oil demand is still near record highs.

Even the IEA, which has the earliest peak demand forecast of any major energy agency, sees demand growing through the end of the decade before flattening. Not collapsing, flattening.

And ironically, the underinvestment driven by ESG restrictions has created the very supply constraints that will support higher prices.

The market seems to be pricing energy as if the transition is already complete. It isn’t.

Meanwhile, energy is already the best-performing sector YTD in 2026, up nearly 23% through February 11. (Source)

This might just be the start.

2026 Is a Midterm Year

Here’s another wrinkle worth considering.

2026 is a midterm election year, and historically, midterm years are the most volatile year of the four-year presidential cycle.

The average intra-year drawdown during midterm years is 19%, compared to just 13% in other years.

The S&P 500’s average price return during midterm years since 1950 is just 5.9%!

Why does this matter for oil stocks?

Because volatility and weaker index-level returns tend to hit the most crowded trades hardest. And right now, the most crowded trade in the market is FAANG. Information Technology alone makes up over 30% of the S&P 500.

When the index goes through one of those midterm year drawdowns, the highest-flying, most overweight sectors tend to get hit the worst.

And money doesn’t disappear: it rotates.

And where does it rotate to?

Historically, it flows toward under-owned, cheap, cash-flowing sectors.

We’re already seeing that.

Think Of The Setup This Way

You have a sector that is:

At a near-record low weighting in the S&P 500.

Supported by a structurally inflationary macro environment.

Entering a midterm election year, historically the most volatile and weakest year of the presidential cycle, which tends to punish crowded trades and benefit cheap, underowned sectors.

Generating massive free cash flow and returning it to shareholders.

Trading at very reasonable valuations.

Already showing signs of a reversal (best-performing sector YTD 2026)

Mean reversion alone, a move from 3% back toward even 5-6% of the index, would imply significant outperformance.

Add in the inflation tailwind and you have a setup where these stocks could legitimately double over the next 3-5 years.

I’m not saying you should go all-in on oil stocks.

But if your portfolio has zero energy exposure, and many don’t, you might be making a bigger bet than you think.

Of course, none of the above is financial advice.

Thanks for reading Playing For Doubles!

Subscribe for free to receive new posts and support my work.